Global macro is getting interesting again

The US and Iran are set to sign a 14 point memorandum of understanding that will restore traffic in the Strait of Hormuz to pre-war levels. It leaves Iran in a better place than before the war as it lifts US sanctions and unfreezes billions of frozen Iranian funds, and it doesn’t even require Iran to give up its uranium. Noahpinion points out how this is a humiliating defeat for Trump and highlights two possibilities that would make this even more embarrassing for the US:

Iran will reportedly start charging fees on transit through the Strait of Hormuz. This is a toll on international shipping — something forbidden by the UN Convention on the Law of the Sea. This will be a huge source of income for Iran — something that didn’t exist before the war.

The U.S. and/or its Middle Eastern allies will reportedly pay Iran a $300 billion reconstruction fund, as well as unfreezing Iranian assets. This is equal to one entire year of Iran’s GDP, and would effectively constitute war reparations. JD Vance has said that the reconstruction fund is not yet confirmed.

I haven’t been writing much about Iran for a while - mainly because it’s difficult to trade and because it mattered less and less for global macro and equities as the war progressed. My Substack and X feeds suggest that a lot of global macro traders (not naming names here) are fighting these moves in oil and equities. I ignored the energy bulls and barrel counters because it was clear to me that they were missing key pieces of how global energy supply and demand would rebalance to make the energy shock less acute than it could have been.

I pointed out in my recent Realvision interview how you can’t underestimate the ingenuity and resourcefulness of the global energy industry to adapt to the SoH shock. We are only finding out now that the US was sneaking out barrels using ship-to-ship transfers. Doomberg also points out how China was the pivotal and unexpected variable in rebalancing supply and demand. China is also a black box that is hard for barrel counters to measure:

That China has the ability to swing 3 to 4 million barrels per day of crude demand for months at a time without a flinch seems a profoundly important development. Without knowing the specifics of how this was accomplished, one can conclude that sufficient engine switching and demand-shifting capacity exists within the country to cap oil prices in all but the most extreme scenarios. This has clearly been done, within factories and consumer products alike, on a scale few have yet fully internalized.

As we have often pondered both here and on numerous podcast appearances, if $150 oil prices could not be achieved with the Iran war fact set, how could they ever be achieved—at least in real US dollar terms?

Said another way, if crude oil has shifted from a necessary hydrocarbon to an optional one at the margins, and those margins are as wide as Chinese demand, what does the future entail for energy prices?

There has been some recent debate about how open source and cheap models will commoditize intelligence. This debate is not new - we were discussing the exact same thing when Deepseek first came out. What the AI naysayers missed is that consumption of tokens is increasing by 1-2 orders of magnitude per year and growing the pie for everybody. A lot of people also underestimated how much of a dollar premium frontier intelligence can command over open source and lagging edge models. The size of the price premium should follow the size of the gap between the capabilities and user experience of frontier intelligence vs open source. Dario Amodei believes the gap between frontier intelligence and open source will widen due to recursive self-improvement. For now, the race is still too close to call.

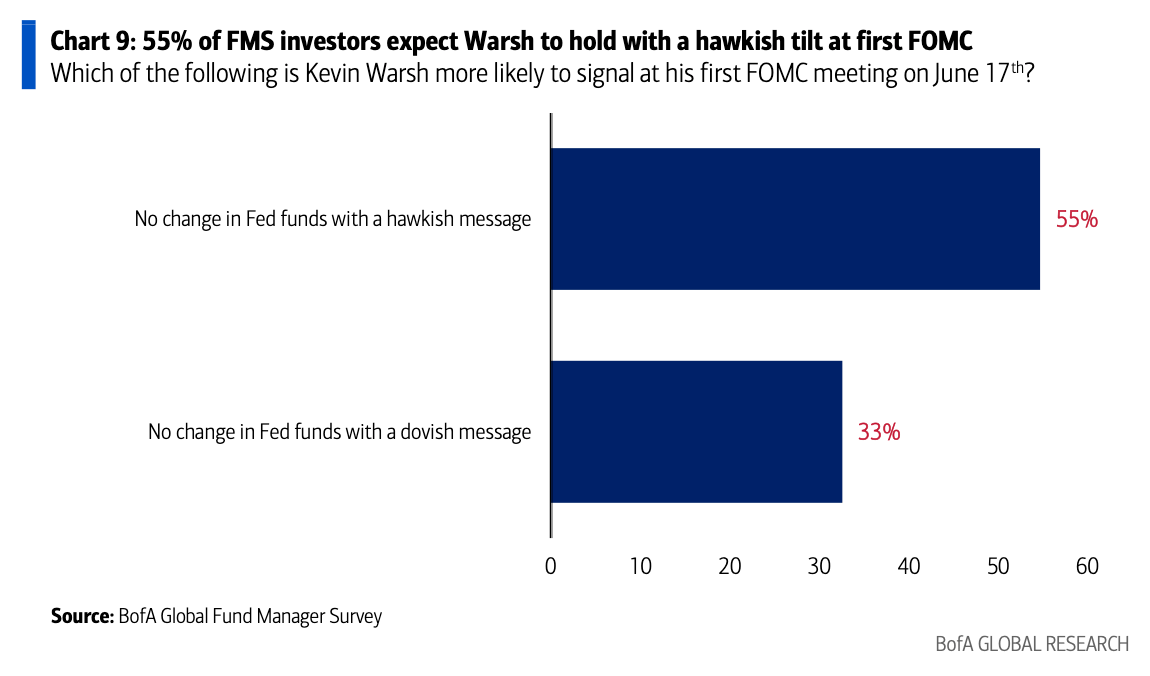

We’re getting a new Fed chair today! I think the market will walk away from tonight’s meeting believing that the Fed will be on hold for a while - a slightly dovish outcome. Warsh’s previous tenure at the Fed and public comments suggest that he holds dovish views during Republican administrations and hawkish views during Democrat administrations. I believe his current tenure will be no different, as Trump would not have brought him in if he didn’t believe Warsh was aligned with the White House. Warsh is also citing the Dallas trimmed mean as his preferred inflation measure - a figure that stands at 2.3% and is one of the lowest of all the alternative inflation measures that the Fed looks at.

The market disagrees with me despite the fact that the supply shock from Iran and the price shock from tariffs are dissipating. Perhaps there’s a trade here.

What will be even more important to watch out for is how the Fed’s signaling and reaction function will change under Warsh. He may decide to remove the dot plot and provide less color on the internal discussions of the Fed in the official Fed statement. Powell rarely delivered an outcome that deviated from market pricing when he was chair, which made the Fed predictable and dampened volatility. Warsh may introduce more uncertainty into Fed meetings and increase volatility during his tenure.

Paid subscriber section: New additions and removals from the AI portfolio, and a new global macro trade