AI vibe shift, broad market views

Markets have been choppy over the past couple weeks, and ever since I exited my entire AI portfolio, I’ve been enjoying some time off traveling with my family. The trigger for exiting was a nagging sense of a coming Minsky moment and a looming vibe shift. Since then, the narrative around AI lab revenues and capex has deteriorated further. When you have markets as speculative and unanchored as what we have seen in semis, the main driver of prices becomes solely narrative and positioning.

If I had to break down the vibe shift, it would consist of the following:

Meta is building a cloud business to rent out its compute, which will increase overall supply of compute and challenges the narrative that compute is structurally supply constrained.

OpenAI is considering delaying its IPO until next year. OpenAI relies on fundraises at ever increasing valuations to fund its insatiable demand for compute, so its struggle to raise funds will trickle down to the semiconductor supply chain.

AI labs are figuring out how to lower inferencing costs, therefore reducing demand for compute. This requires Jevon’s paradox to work in overdrive as token consumption needs to increase by a larger magnitude just to keep demand for compute stable.

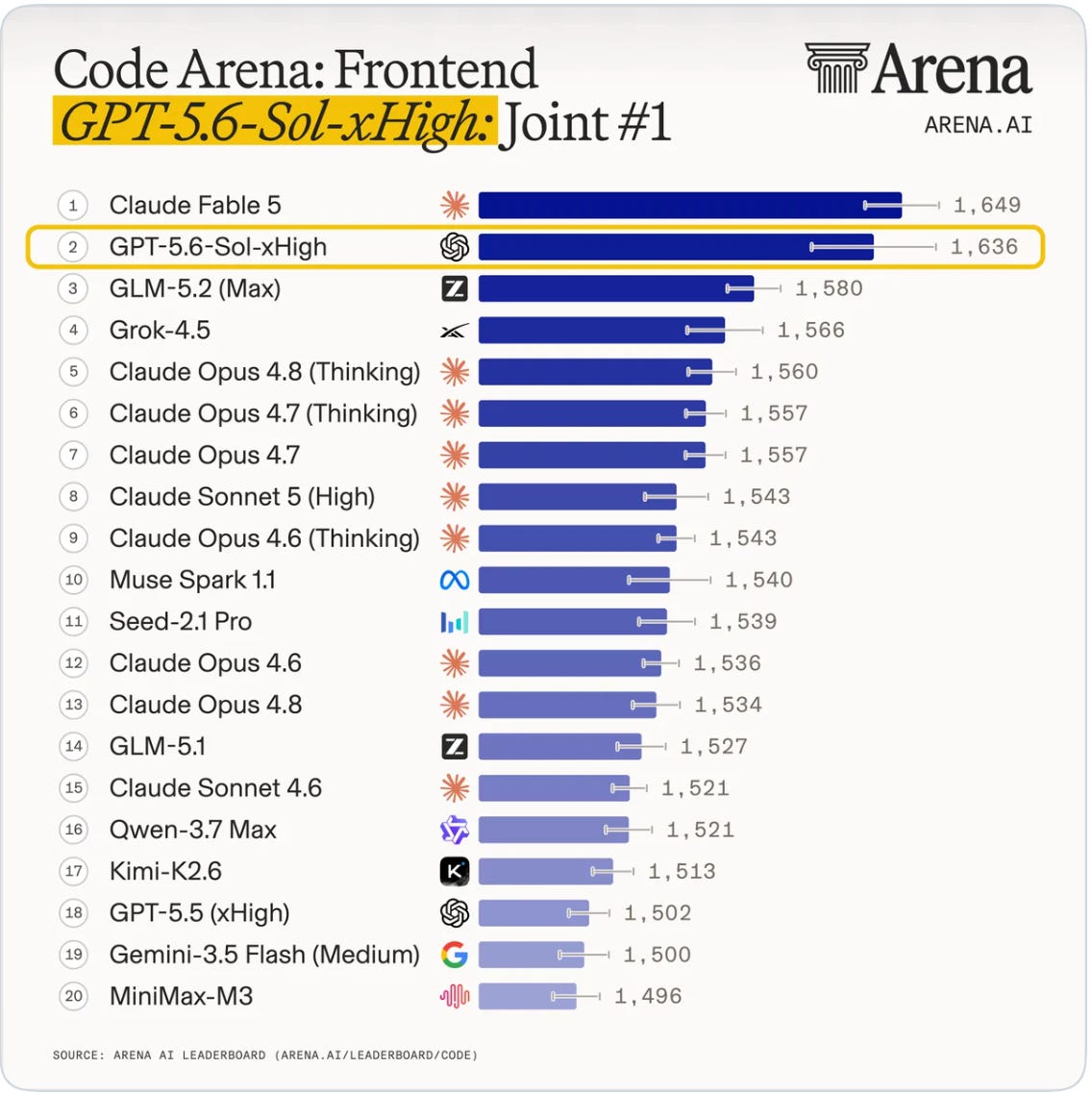

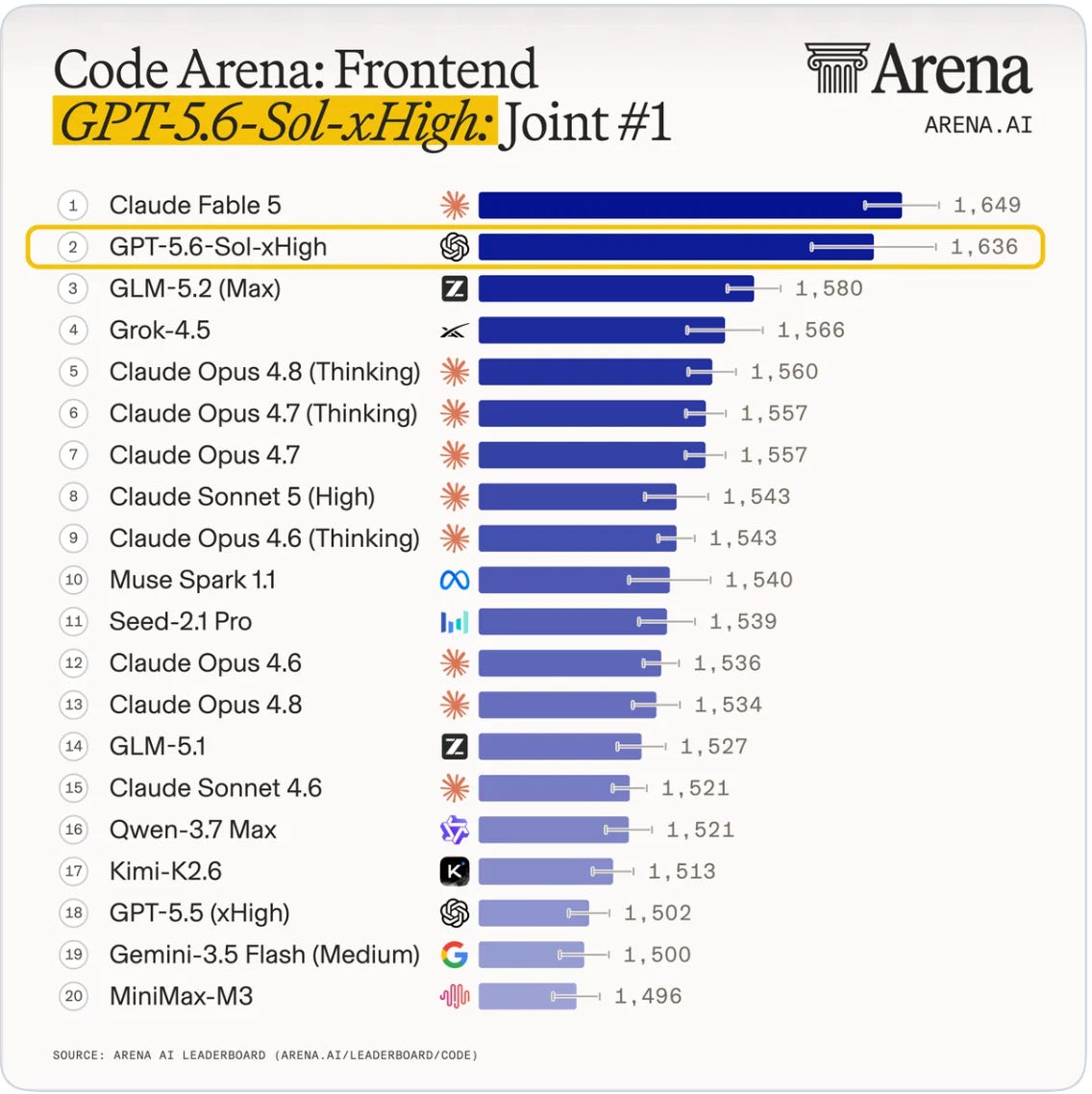

Intelligence is bunching at the frontier, resulting in fierce competition which should lead to margin compression of model lab revenues. SpaceX launched Grok 4.5 and OpenAI launched GPT-5.6 Sol, both of which score in the top five on Code Arena. Meta just released Muse Spark 1.1, a coding and agentic model that falls short of the top five but is priced aggressively cheap.

Samsung’s blockbuster earnings produced a news failure: the stock sold off despite beating on revenues and earnings and now trades about 15% below its level on the day of the release.

The conversation is increasingly turning towards token optimization vs token maxxing and questioning the ROI on enterprise AI spending. Chamath Palihapatiya raised this on the latest All-In podcast episode (14:45) and if you listen to the episode in its entirety, you can sense the vibe shift compared to the tone a month or two ago.

Finally, Palantir’s Alex Karp made a widely shared and public rant against how the way AI is currently sold and served by closed frontier labs offers enterprises questionable value while stealing corporate IP and data. Satya Nadella wrote an excellent article “The Reverse Information Paradox” suggesting that enterprises need to bring their models in-house rather than sharing their institutional data and knowledge with closed frontier labs. Taken together, these signals point toward a future in which AI revenues and capex no longer concentrate in a handful of labs, but instead disperse across a “Cambrian explosion” of private AI stacks, where governments and major corporates run their own compute, models, harnesses, and data.

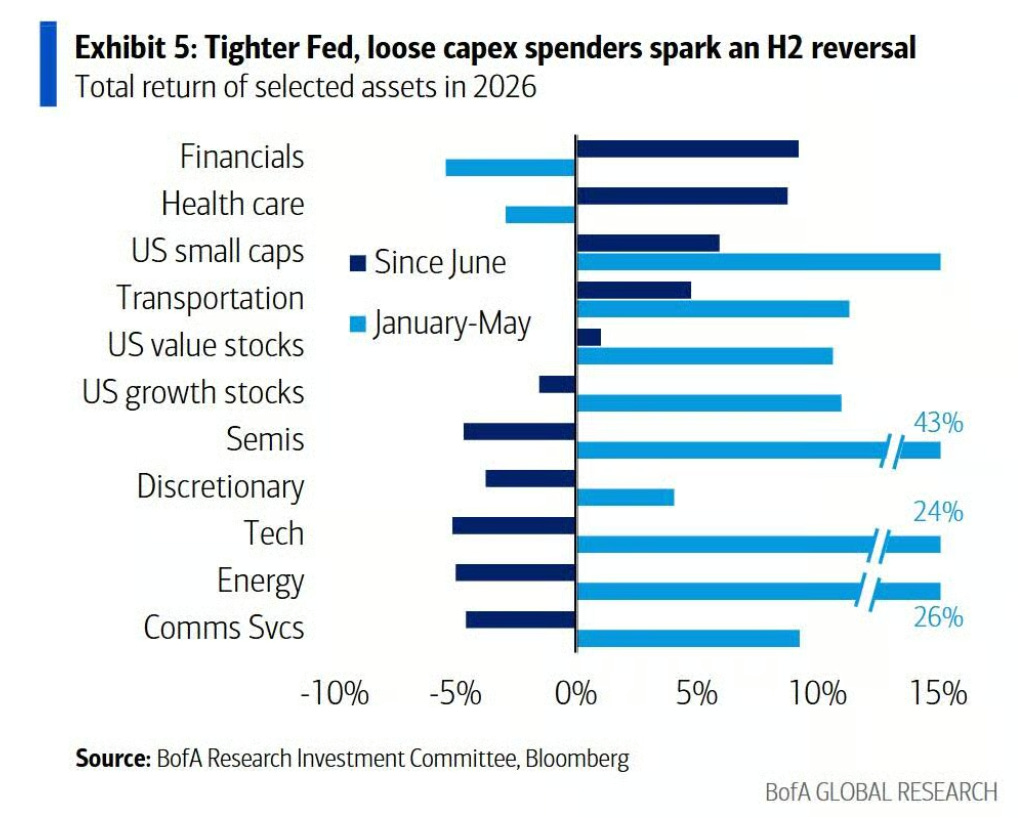

Where does the AI semis and infra sector go from here? I see a lot of speculative excess that still needs to unwind, with equity supply set to rise as new IPOs come to market and SpaceX shares unlock. My base case is a multi-month topping process, so I have little appetite to re-enter the trade. I remain convinced that AI will reshape the economy over the long run, yet picks-and-shovels booms in history have usually been cyclical rather than open-ended secular growth stories. Capital already appears to be rotating into areas like healthcare, software, and biotech. With the initial picks-and-shovels phase fading, the next challenge is sorting out the eventual winners and losers as AI diffuses through the broader economy.

The return of stagflation fears

Tensions have reignited in the Strait of Hormuz as Trump and Iran have gone back to exchanging fire, and Trump has reestablished the US naval blockade of the Strait. The ceasefire has collapsed and Brent crude oil has rallied from a low of 70 back up to 85. The main point of contention remains Iran’s control of traffic through the Strait - something the US and the rest of the world is unwilling to accept.

Interestingly, Iran resumed attacks on vessels on July 9 - the day of Khamenei’s state funeral. This suggests that the hardliners in Iran are still in charge and are seeking revenge on the US. The likely outcome is a long-term “on again off again” war that periodically flares and then cools.

With cracks appearing in the AI trade and a Fed concerned about sticky inflation, a spike in oil prices is the last thing the market needs. Despite recent headwinds, the broader index is behaving rather sanguine, which makes me wonder if we will see a pullback in risk sometime this quarter. I’m currently sitting on a lot of cash in my long-term portfolios and am accumulating gold into weakness, as precious metals are now bombed out and left for dead. The debasement narrative went from being a huge theme in global macro to being hardly talked about at all, but anyone who has traded global macro long enough knows that it will return at some point.

My trading book is clear of positions - but there’s one tactical setup in rates that I am watching today. More in the paid subscriber section.