Turning neutral on AI semis and infrastructure

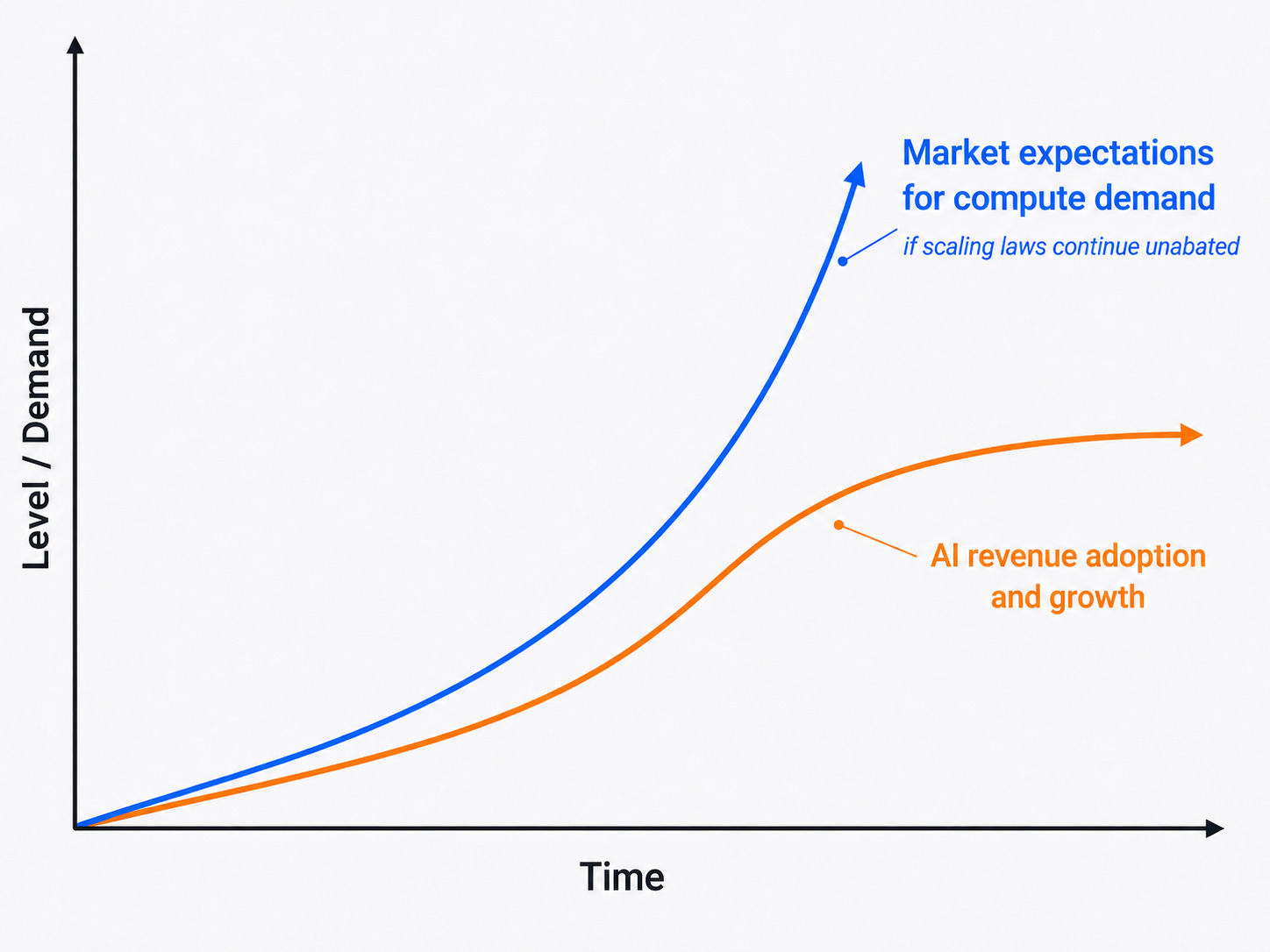

I had a vivid dream last night in which I unwound my entire AI portfolio. In the dream, I saw a parabolic line shooting higher that represented the market’s expectations for how much compute would be required if scaling laws continued unabated. Alongside it was another line that also trended upwards but at a slowing pace. This line represented the speed of adoption and growth of AI revenues. I realized that economic reality would eventually collide with the market’s over‑extrapolation of AI scaling laws, and that realization made me hit the sell button across my entire portfolio in the dream.

I woke up unsettled and picked up my phone to check the market. Most names were in the green, so nothing seemed alarming at first. I still could not shake off the dream, because I rarely dream about markets and the rationale for selling in the dream echoed a concern that has been gnawing at me over the past week. Every technological revolution follows an S‑curve. As I went about my day, the question stuck with me: are we nearing the end of the steep part of this S?

Perhaps the dream did foreshadow something, because the Korean Kospi sold off 10% today. The Kospi has become the epicenter of AI speculation, with memory chip makers Samsung and SK Hynix making up 52% of the index. Korean speculators have piled into AI 2x and 3x ETFs with reckless abandon, creating hidden leverage through options convexity in the underlying. The price action confirmed my gut instinct, and I decided to unwind my portfolio. Most of my names will not trade until the US open, so I will be busy hitting the red sell button tonight.

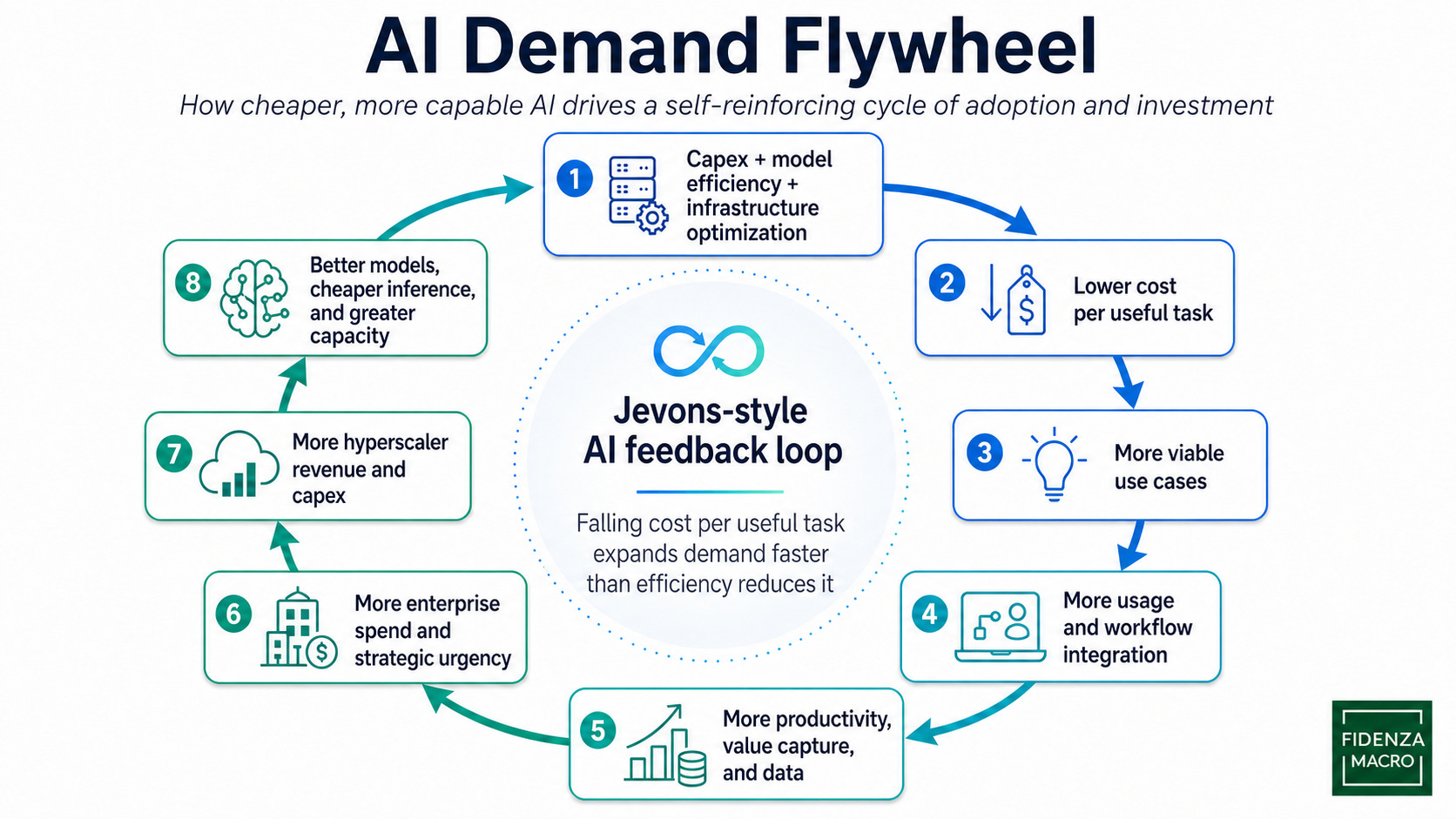

The Jevon’s Paradox-fueled AI flywheel is what previously made me bullish. As long as this flywheel keeps spinning, I would stay long, but anything throwing a wrench into it would cause concern.

Earlier this month I wrote about the six main threats to the AI boom:

Commoditization of AI

AI safety becomes a roadblock to progress

Users balking at full unshackling or unhobbling (providing full access to AI)

Too much equity supply

Stagflationary shock

Political and social opposition to AI

Threats #1 to 5 have gotten worse, and #6 worries me in a different way from what I originally imagined.

Commoditization of AI

June 9

Today, users are flocking to frontier models at Claude and OpenAI and paying top dollar because they believe the quality gap and ROI justify the cost. This supports high gross margins and explosive top‑line growth, which in turn fund massive compute budgets. That loop may not last forever.

Routing and orchestration are getting more sophisticated as developers try to manage inference costs. Open source and non‑frontier models are improving quickly, and there is a credible path where, within a year or two, they are “good enough” for the overwhelming majority of workloads. If 80–90% of tokens shift to cheaper, near‑frontier or open‑source models, the revenue pool at the very top of the quality spectrum could end up much narrower than current capex plans assume.

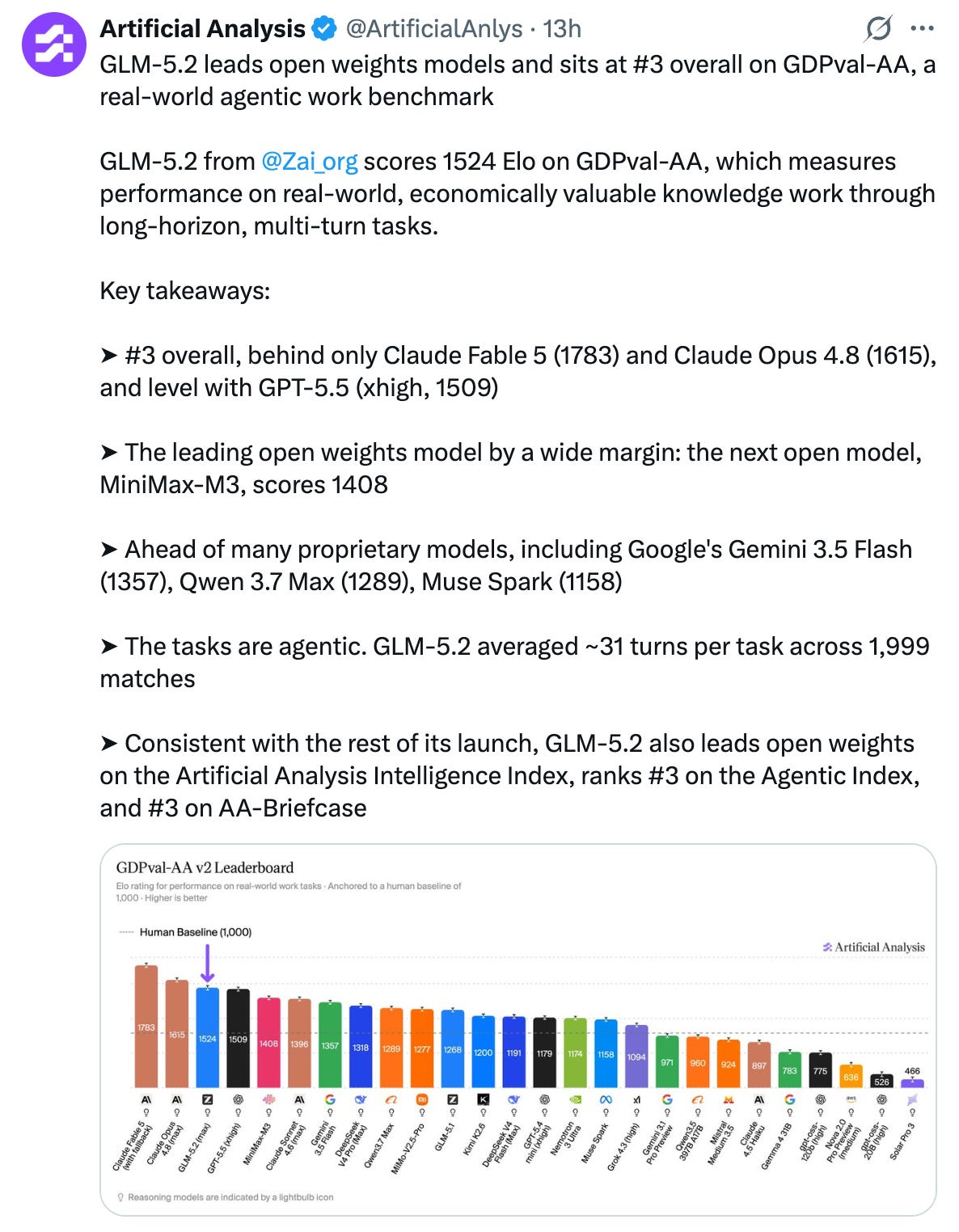

What worries me is that during the ten days while Fable has been sitting on ice and banned by the US government, we’ve seen two releases of cheaper models that claim to rival Fable in performance. The first is Chinese AI lab Zai’s release of 5.2 - an open-weight model that excels at agentic and long horizon tasks and comes close to Fable and GPT 5.5 in capabilities.

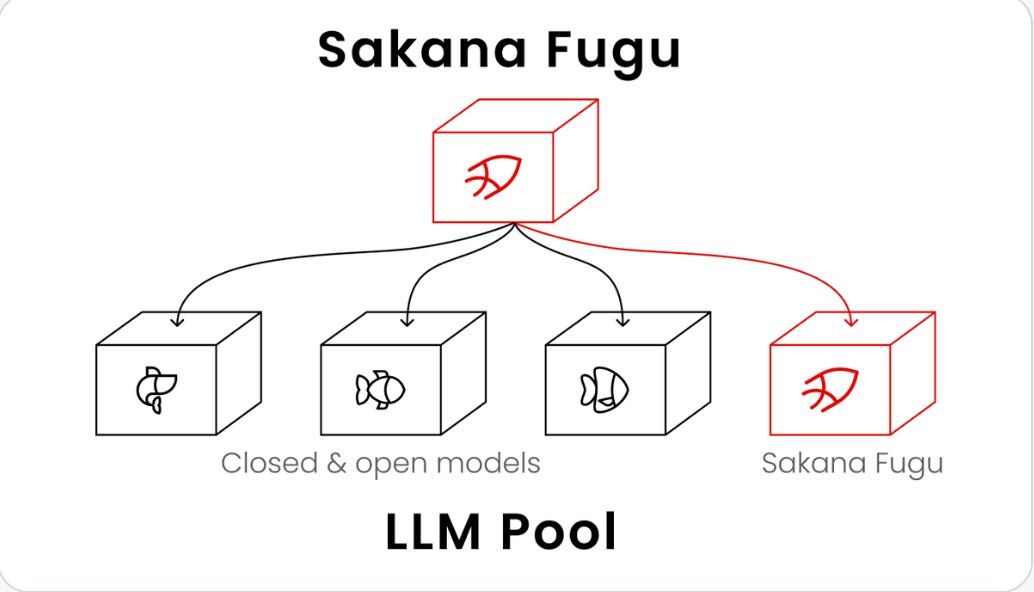

The second release was Fugu, a multi-agent orchestration system created by Sakana AI from Japan. This product uses a mixture of models to achieve near-Fable performance.

Competition is closing in from all directions (even Japan of all places!) and what’s scary is that these smaller labs are using novel methods to reduce training and inference costs.

Zai’s GLM-5 paper:

First, we adopt DSA (DeepSeek Sparse Attention) [9], a novel architectural innovation that significantly reduces both training and inference costs. While GLM-4.5 improved efficiency through a standard MoE architecture, DSA allows GLM-5 to dynamically allocate attention resources based on token importance, drastically lowering the computational overhead without compromising long-context understanding or reasoning depth. With DSA, we scale the model parameters up to 744B and extend the training token budget to 28.5T tokens.

Sakana.AI’s website boasts that RSI is in the company’s DNA:

Sakana AI is one of the earliest labs developing Recursive Self-Improvement (RSI) technology using modern foundation models. Today, we are proud to announce the formal establishment of the Sakana AI RSI Lab, a dedicated research group within Sakana AI, tasked with redesigning the AI development process itself with AI.

By transitioning from static, human-led R&D to autonomous, self-improving intelligence engines, we are turning constraints into our greatest compounding advantage. We are building the definitive architecture for the next frontier of AI.

Wait a minute, wasn’t Anthropic’s Amodei the one who said that recursive self-improvement would help frontier labs accelerate advances in AI? Ironically, RSI is helping smaller and nimbler competitors as much, if not more.

How does this affect the AI demand flywheel? Competition from open source or cheaper models eats into Anthropic and OpenAI’s margins, preventing them from committing to future compute. It also increases the risk that they overcommit to compute and end up being on the hook for compute without the revenues to pay for it. I had previously warned that a slowing of Anthropic’s revenues would be a sign that the AI boom is rolling over, and competition from cheaper models certainly makes that more likely to happen.

AI safety becomes a roadblock to progress

Recent events have shown that models can no longer become more powerful without also posing a threat to society and inviting government regulation and scrutiny.

This is the “safety wall” that I was talking about in my previous post, and the fact that we have arrive so quickly at it is concerning. The fear of Mythos causing economic and political damage exceeds the excitement and potential for AI to create real economic value. This fear will limit the usefulness and reach of next-gen models while allowing open source and foreign AI labs to catch up to the US.

Users balk at full unhobbling and social opposition to AI

In conversations with non‑profit leaders, I hear persistent resistance and concern about bringing AI into their organizations. Most companies and institutions still lack a formal AI policy and budget that spell out how to use AI safely and how much they can spend on it. Their hesitation rests on both social aversion to AI and legitimate safety concerns:

June 9

Many individuals and enterprises may be uneasy about giving an AI access to internal files, communications and production systems. Security and compliance teams will rightly demand rigorous controls, and a steady drumbeat of stories about prompt‑injection attacks, data leaks or mis‑executed workflows would reinforce that caution. If users keep agents on a tight leash, AI spend still grows, but average tokens per user can fall well short of the bull‑case “everything is automated” scenario.

The slow speed of diffusion of AI into the broader economy will limit the economic gains companies will derive from AI, and therefore will limit how much companies and individuals will be willing to spend on it.

Too much equity supply

June 9

In addition to the SpaceX IPO and Google equity offering, Meta is considering offering more equity to fund its AI ambitions. Both Anthropic and OpenAI have confidentially filed for an IPO. Over the next year, it is plausible that markets face trillions of dollars in AI‑themed equity supply when you combine IPOs, ATM programs and insider unlocks. At the same time, institutional positioning in AI leaders is already heavy, and large allocators need to manage exposure caps and liquidity risk. Even if the fundamental outlook remains strong, that volume of issuance can weigh on multiples and absorb marginal dollars that would otherwise push prices higher.

Price and valuation are simply a function of how much capital flows into a particular equity or sector. Companies can continue to grow revenues and earnings, but if equity supply outweighs demand, then price will fall regardless of fundamentals.

Stagflation shock

I didn’t expect Warsh to be so hawkish in his last FOMC, but he dropped a surprise hammer on the market and now the Fed funds curve is pricing in a high possibility of a hike by September. With each passing month the AI economy relies more and more on debt and bond financing. If scaling laws continued on their path and the flywheel continued to spin, higher rates would not be as much of a concern. However, all the headwinds I mentioned above have crystallized in a short space of time, which means a hawkish Fed is now one more thing the market needs to worry about.

A few other data points:

Silicon Data’s token expenditure index has fallen sharply. When I last posted about this index at the beginning of this month, this index was at its peak. The pullback reflects a backlash to tokenmaxxing and increased user sophistication in managing token costs and routing tasks. It’s too early to say where this is a pullback or a top.

Silicon Data’s H100 rental price index:

Ornn’s version of the H100 rental price index looks way worse:

I could be wrong about this being an interim top for AI. Maybe the sector pulls back for a few days to weeks and then continues to roar higher. Everything looks pretty bullish at market tops and if you wait for dark clouds to arrive, your portfolio will already be down a lot by then. To get out with perfect timing, you need to be willing to give up on future upside and be a little lucky.

Since I went long AI in April, equities have contributed about 10% to my overall gains on 40–50% exposure. The trade offered a pleasant distraction from the Iran war and gave me something to cheer about while the rest of global macro remained very difficult to trade. I am not ruling out a return to the trade, but I would need to see many of these headwinds clear first.

Disclaimer: The content of this newsletter is provided for informational and educational purposes only and should not be construed as professional financial advice, investment recommendations, or a solicitation to buy or sell any securities or instruments. The newsletter is not a trade signaling service and the author strongly discourages readers from following his trades without experience and doing research on those markets. The author of this newsletter is not a registered investment advisor or financial planner. The information presented on this newsletter is based on his own research and experience, and should not be considered as personalized investment advice. Any investment or trading decisions you make based on the content of this newsletter are at your own risk. Past performance is not indicative of future results. All investments carry the risk of loss, and there is no guarantee that any trade or strategy discussed in this newsletter will be profitable or suitable for your specific situation. The author of this newsletter disclaims any and all liability relating to any actions taken or not taken based on the content of this newsletter. The author of this newsletter is not responsible for any losses, damages, or liabilities that may arise from the use or misuse of the information provided.

quite interesting how few comments this one has

I feel like the impact of rate hikes specifically on AI company solvency is overstated, when you look at the largest debt holders it's really just Oracle, who while being critical for OpenAI isn't anywhere close to backstopping the entire market.

Also we haven't really seen huge market share takeover by open-source models which leads me to believe they are still lacking something fundamental. My talks with the AI crowd in SF indicate that most industry people think that stuff like GLM is just benchmark maxing and doesn't actually have the holistic capability that Claude has.